Advanced Risk Delineation and the Insurance Industry

Advanced Risk Delineation and the Insurance Industry

TerrainWorks (NetMap) new data and technologies could impact property and casualty insurers in at least three ways.

Improved Justification for Claims

Advanced environmental risk delineation could increase insurers’ exposure to claims for indemnification of settlements and judgments in cases against insureds for causing environmental harms. For example, as availability of new risk data increases the abilities of governmental agencies and private actors to recognize cause and effect in environmental events, courts will be more likely to impose liability on those who could have used such data and technologies to avoid or mitigate those risks. As they do, demands for indemnification from P&C carriers will likely increase.

More Effective Pricing of Policies

Pre-loss use of new risk data by actuaries could enable more accurate assessment of environmental risks underwritten through existing types of property and casualty insurance, allowing carriers to refine their selection and pricing of new and renewal business on their existing lines of coverage in their current operating regions. This is apparent as older coarse grained risk assessments are superseded by detailed risk mapping. See Real Estate Transfer of Risk

Pre-loss use of new risk data by actuaries could enable more accurate assessment of environmental risks underwritten through existing types of property and casualty insurance, allowing carriers to refine their selection and pricing of new and renewal business on their existing lines of coverage in their current operating regions. This is apparent as older coarse grained risk assessments are superseded by detailed risk mapping. See Real Estate Transfer of Risk

Increasing the Insurance Market

Third, use of new data and technologies by actuaries could facilitate carriers’ entry into new product and geographic markets for which they have previously lacked sufficient information to make sound actuarial decisions. For instance, simply the proliferation of advanced environmental risk maps will increase liabilities for all parties, including for example liabilities caused by newly acquired real estate, in both rural and metropolitan areas.

TerrainWorks: Increasing Access to Risk Locality Data

Actuarial predictions, a science already exposed to large uncertainties, are becoming increasingly ambiguous due to the non-stationary statistical properties of climate change. The increasing uncertainty in predicting extreme event probabilities is occurring, fortuitously, with a coincident increase in the availability of high-resolution environmental risk locality data.

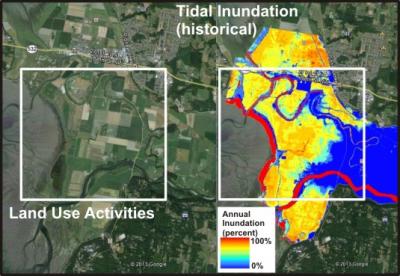

In the last decade, increasing access to high-resolution spatial information (related to topography, climate, vegetation, roads, soils, and satellite imagery) combined with new computer technologies and natural science models is providing unparalleled mapping of environmental risks involving wildfire, landslides, mudflows, coastal flooding, and climate change, among others.

Additional high-resolution spatial data include the ecologically critical habitats of rivers, floodplains, and estuaries and their associated threatened and endangered species. Such “risk locality” data overlaid onto maps of homes, highways, and animal habitats enable unprecedented identification of environmental liabilities. Increasing availability of high-resolution risk locality data over large geographic areas is an asset to the environmental insurance industry, including reinsurers, and to insureds.

The Growing Challenge in Actuarial Science

From an actuarial perspective, there are two sides of the coin regarding hazardous events. One side involves predicting the probabilities of extreme events. Here, the actuaries must quantify the tail of highly-skewed distributions, which is challenging given short historical records and our imperfect knowledge of natural systems. Compounding this issue is the increasing uncertainty driven by a changing climate. Increasing global warming is likely contributing to a more dynamic climate in which historical records are becoming less useful in forecasting the future and where a non-stationary climate renders forecasting highly inaccurate (Ranger and Niehörster 2012, Niehörster et al. 2013).

In addition, the very approximate nature of global climate models (GCM), and in particular, the challenges involved with downscaling GCM predictions to particular geographic locales (Chen et al. 2011), render the inclusion of GCM predictions into actuarial extreme event forecasting problematic at best and will result in significant uncertainties.

The flip side of the coin involves the locations of hazardous events or environmental risks. Unlike the increasing uncertainty and ambiguity in predicting extreme event probabilities (Walker and Dietz 2012), new science and technology are greatly increasing the spatial resolution and detection of the localities of extreme events and environmental risks. Although the deterministic locality in the landscape is strongly linked to the probability of an extreme event, vis-à-vis the stochastic climate, the physical location (locality), by itself, can provide very useful information in which actuaries can consider the relative exposure to extreme events or environmental risks.

The flip side of the coin involves the locations of hazardous events or environmental risks. Unlike the increasing uncertainty and ambiguity in predicting extreme event probabilities (Walker and Dietz 2012), new science and technology are greatly increasing the spatial resolution and detection of the localities of extreme events and environmental risks. Although the deterministic locality in the landscape is strongly linked to the probability of an extreme event, vis-à-vis the stochastic climate, the physical location (locality), by itself, can provide very useful information in which actuaries can consider the relative exposure to extreme events or environmental risks.

TerrainWorks (NetMap) focuses on identifying risk localities rather than risk probabilities because of the complex nature of defining probabilities of storms, wildfires, erosion, and floods and because of the lack of location-specific data that would contribute to accurately assigning probabilities of extreme events. For example, to predict the probabilities of mudflows following wildfires would require detailed information on soil volume mantling hillsides as well as vegetative rooting strength, a level of spatial information that is not obtainable in the foreseeable future. In addition, combining co-dependent probability distributions, say in the case of wildfire followed by extreme precipitation, remains a significant challenge, one that is exacerbated in the face of a changing climate.

Contact us for additional information on how spatially explicit information on environmental liabilities can provide new and cost effective opportunites for the insurance/reinsurance industries. Read more: Risk Transfer Analysis